Five Credit Score Myths That Can Cost Financial Mishaps

Bad credit scores can really hurt” is an understatement. Back in the day, these determine a person’s qualification for a loan. Now, credit scores can influence employers in their hiring decisions and benchmark for insurance rates.

CC Image By Casey Konstantin From Flickr

Whether you have accumulated surmountable credit card debts, filed for bankruptcy or missed a few payments, your damaged credit score could potentially make it even harder for you to recover from losses.

It’s quite impossible to survive without credit scores, at least in the United States. Unless, you have guaranteed pocket full of cash all the time, by all means, you can let go of obtaining one. Not being able to build a credit history is another obstacle standing in your way.

Responsible approach to managing personal finances is the cornerstone of pristine credit scores. But, what if you have taken missteps in your life? Is this the end for you? There are commandments to live by, and there are also myths that should be discarded from the memory bank.

These five urban legends of credit rating can easily derail your financial well-being. Myths can be fun sometimes, but not when money is involved.

1. My credit score will plummet as I proactively do spot checks.

You have nothing to lose. The inertia linked with regular credit score check-up is oftentimes the barrier of maintaining a sound credit health. Conducting a self-check will cause short-term fluctuation, but will have zero impact on your credit score.

By doing this religiously, you can easily spot red flags on your credit behavior. Some consumers tend to be careless over an outstanding credit score from the previous year, not knowing that a single mistake can turn a prince into a frog in a snap.

While obsessing with credit rating is not healthy, checking it at least once a month will give you a glimpse of your credit health over time. This will allow you to control spending behavior and see whether there are erroneous or fraudulent activities happening that are beyond your knowledge.

Credit monitoring services provider such as creditflare.com empower consumers to manage their credit habits and scores.

2. FICO is the only true standard of credit scores.

FICO stands for Fair Isaac Company. A FICO (3-digit) score can be affected by several factors including amount of debt, payment history and other variables. But, this is not the only true standard of credit scores. In fact, there is none.

There are a handful of models being utilized by credit bureaus. A model is tailored for particular industries such as mortgage and auto insurance. But, the disparity from one model to another is not that enormous (around 5 to 50 points difference). You could probably be in the same risk range across the entire spectrum.

3. My credit score is like a tattoo, it’s forever.

CC Image By Jhong Dizon From Flickr

Whoever tells you that your credit score will define you for the rest of your life, is either joking or completely ignorant. Credit rating is a reflection of an individual’s credit behavior at a given point in time. It can fluctuate (increase or decrease) dramatically if there is a significant change in your credit report.

Most credit card issuers normally send updated information to bureaus within a period of 30 days. Around two-thirds of credit scores can change as much as 20 points within just 3 months or 90 days.

There is no good in goodbye. But, when you speak of letting go of displeasing credit scores, there will surely be galactic joy.

4. My personal credit profile will be unaffected by business debt.

Business credit card applications and loans will require guarantees from executives, partner or owner by providing his or her social security number. Any delinquency will show up in the credit report of a guarantor.

5. Credit card companies always have the last say.

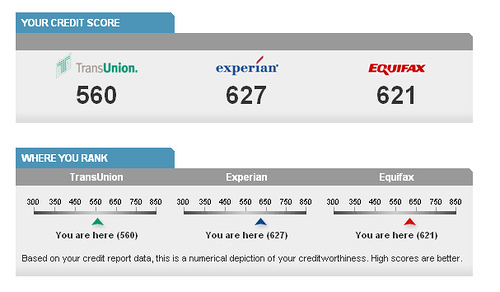

While information largely come from credit card companies and financial institutions, an individual is always given the right to dispute inconsistencies and inaccuracies in his or her credit report to any of the three credit bureaus (TransUnion, Equifax and Experian). There are certain protocols governing resolution of such complications.

Don’t fall for these myths, as simple as that. And by the way, pay your bills on time to free yourself (and your family) from being haunted by poor credit rating in the future.

It’s Your Turn

Are you confident that your recent auto loan will be approved? Have you experienced sleepless nights because of poor credit scores? What have you done to recover?

Share your stories, insights and lessons. Let your journey be a learning ground for others. Drop a note or two at the comment box below.

Author Bio:

Stella Kessler is a full time writer Before that he was seller at a local shop and selling Panasonic tx-l47dt65b LED TV. While he is not writing, he is drawing science infographics.

Share this:

Category: Credit Score